Grid Bypass: The Unregulated Rise of Onsite Power Generation at U.S. Data Centers

How Northern Virginia's data centers are building their own grid — and who pays for the one they're leaving behind.

During the summer of 2025, a fire at an electrical substation in Loudoun County forced dozens of data centers in Northern Virginia onto their backup diesel generators. Some facilities ran diesel for seven hours a day over three consecutive days. One facility, Compass Datacenters’ True North facility in Leesburg, ran its emergency generators continuously for six days and nights. Residents reported visible black smoke from numerous data centers across the county.

The same week, a heat wave pushed PJM Interconnection — the grid operator covering 13 states and 65 million people — to issue Maximum Generation Alerts and activate emergency demand response programs across the Mid-Atlantic, as grid conditions deteriorated to levels requiring DOE emergency orders to keep aging power plants online.

The incident was not an anomaly. Ten miles southeast, in Sterling, a Vantage Data Centers facility had already found a more permanent solution. Vantage II (VA2) has been running on jet turbine power plants, using natural gas, as its primary energy source — not as backup, but as baseload generation — for nearly a year.

Source: Vantage Data Centers.

Local residents reported that the turbines produce a constant 2-kilohertz high-pitched tone audible from more than 1,200 feet away, 24 hours a day, 365 days a year. Nearby residents report headaches, sleep disruption, and wildlife displacement.

Vantage II is not on the grid. It is the grid.

And it is not an isolated case. Across Loudoun County — Northern Virginia’s main data center cluster, with approximately 200 operational facilities consuming over 5.5 GW of electricity, with demand growing at roughly 1 GW per year — data centers are systematically bypassing the utility grid. They are doing it with diesel generators, natural gas turbines, and acquired power plants. They are doing it because Dominion Energy’s power delivery timeline for facilities over 100 MW has stretched from 3–4 years to 4–7 years, with some sites facing waits of up to 17 years. They are doing it because PJM’s own capacity auction failed to meet its reserve standard, and the grid operator has started using the words “brownout” and “blackout” in its planning documents.

And they are doing it in a regulatory vacuum. Virginia’s Department of Environmental Quality (DEQ) classifies onsite data center turbines as “minor” pollution sources. The State Corporation Commission (SCC) has no authority over behind-the-meter generation. Local governments have no established authority to consider energy availability in land-use decisions. Virginia HB 1112 would have granted localities in Planning District 8 the power to deny data center applications where electric energy is insufficient — but after its enforcement provisions were stripped in committee, the bill was continued to the 2027 session.

The result is a shadow power system that is neither metered at the grid level, regulated for aggregate emissions, nor subject to the land use review process that governs every other aspect of data center development.

I. The Grid Delivery Crisis

The core driver of onsite generation is not ideology or preference. It is math.

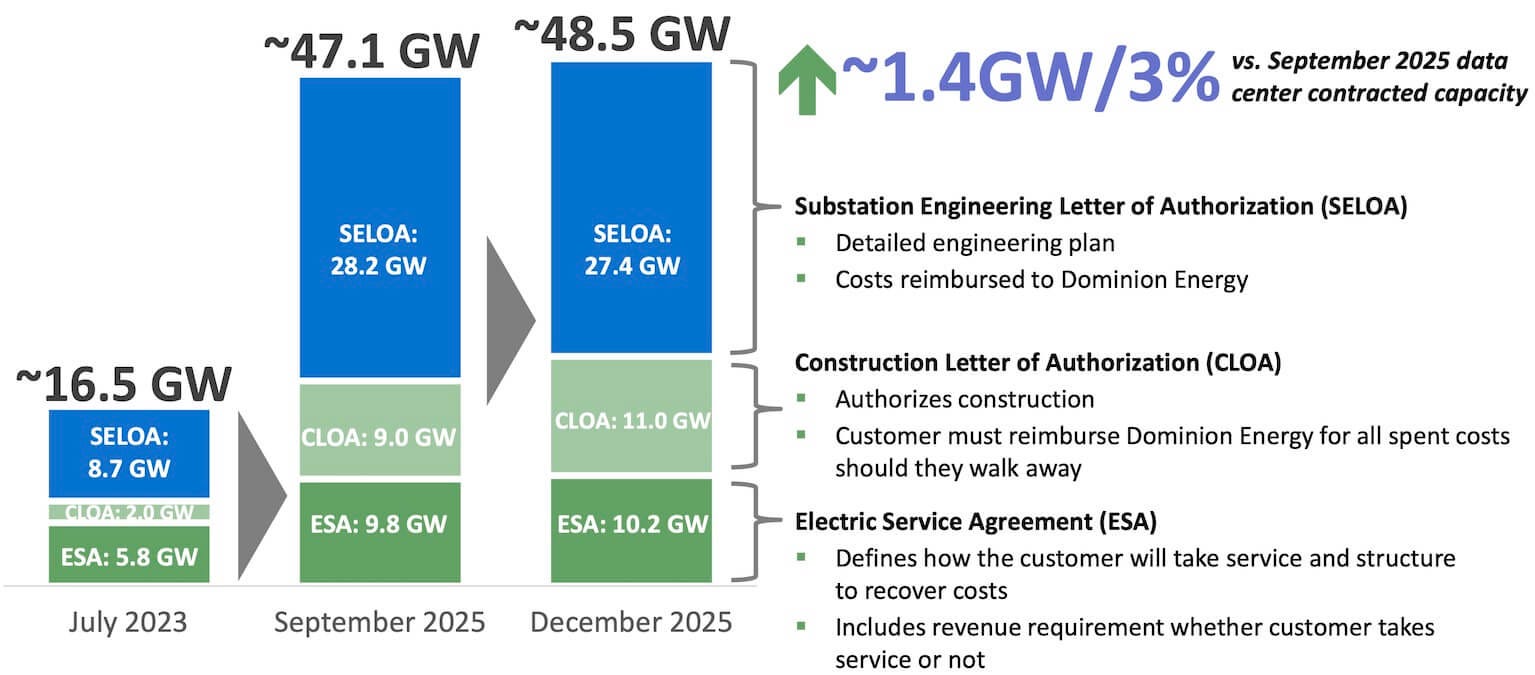

Loudoun County’s electrical demand grew more than 5× in the 7 years between 2018 and 2025, from 1 GW to 5.3 GW. Current demand stands at over 5.5 GW and is growing at roughly 1 GW per year, with projections reaching 8 GW by 2028 and potentially 13 GW by 2038. AI server racks — which typically operate at 40–80 kW per rack, roughly 5–10× the power density of conventional enterprise racks — are accelerating the trajectory. The scale of the mismatch is best captured not by forecasts but by commitments: as of December 2025, Dominion Energy reported approximately 48.5 GW of contracted data center power in its territory.

Dominion Energy Virginia — Data Center Contracted Capacity

Source: Dominion Energy.

The grid cannot keep up. Multiple new transmission lines are under construction in Loudoun County and will not be sufficient. All existing transmission rights-of-way are full to capacity. Dominion Energy confirmed that all data centers over 100 MW can expect full power delivery timelines of 4–7 years (up from 3–4 years previously); county officials have cited Dominion’s own statements that some sites could wait 17 years.

The most ambitious attempt to compress those timelines is a project to develop a 525 kV high-voltage direct current (HVDC) line. Dominion has proposed a 185-mile HVDC line from Brunswick County in southern Virginia to the Mosby substation in southern Loudoun County, delivering 3–4 GW of new transmission capacity. But even under the most optimistic timelines, the capacity would not arrive before 2029–2032.

The regional picture is equally strained. PJM’s 2026 Long-Term Load Forecast projects the Dominion zone as still PJM’s fastest-growing, with 5.4% compound annual summer peak growth and home to roughly two-thirds of all PJM data center load.

PJM Load Forecast Report — Dominion Virginia Power Zone

Source: PJM.

Data center load adjustments across the zone’s utilities — Dominion Energy, NOVEC, REC, and ODEC — total over 7 GW of demand in 2026, rising to 39 GW by 2046. Notably, PJM’s new firm/non-firm methodology derates speculative projects, yet classifies Dominion Energy’s entire data center pipeline as “Firm” given its full backing by electric service agreements and construction commitments.

Across PJM’s full footprint, summer peak demand is forecast to reach 222 GW by 2036 — up from the 210 GW by 2035 projected in the 2024 forecast — reflecting 3.6% annual growth driven overwhelmingly by data center load, which appears as the primary growth factor in nearly every PJM zone.

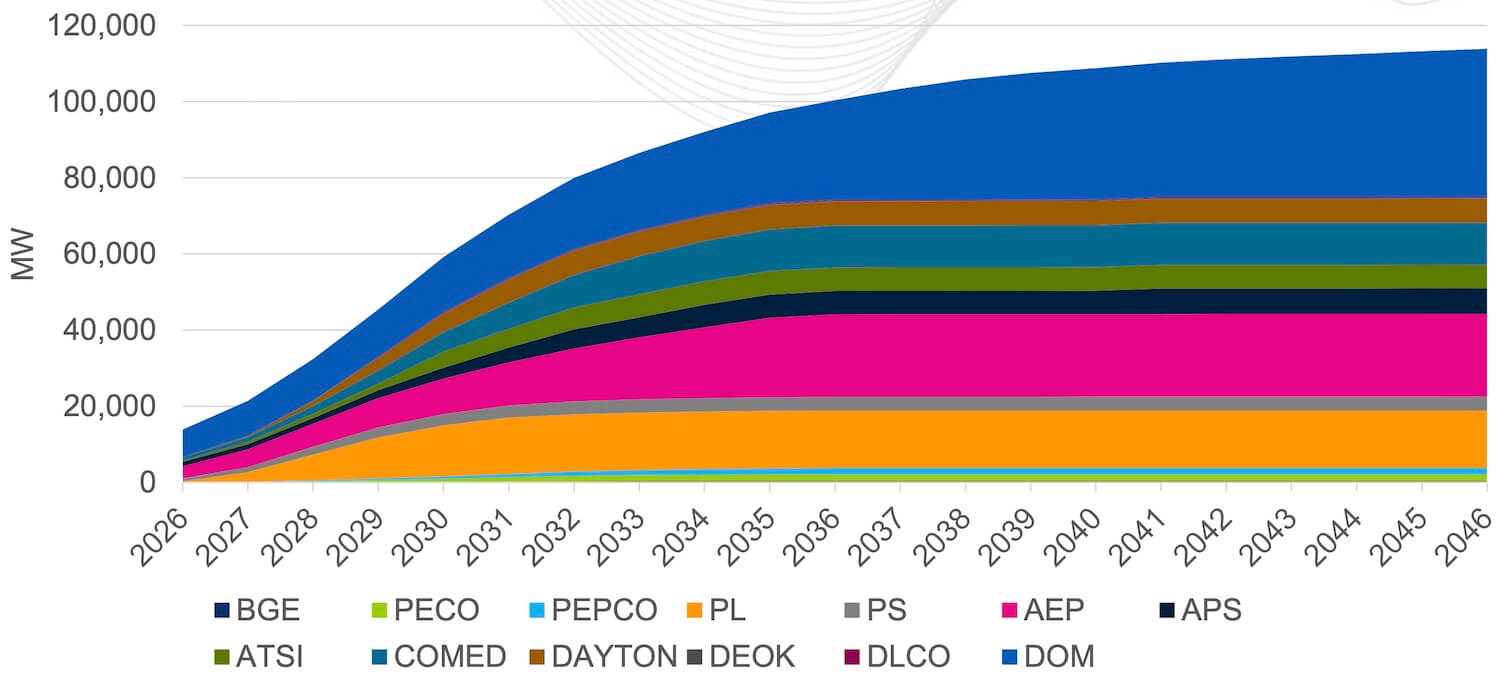

Large load adjustment requests filed with PJM total roughly 60 GW of incremental demand by 2030 and 99 GW by 2035, with data center projects accounting for the vast majority.

PJM — Summary of Large Load Demand Requests

Source: PJM.

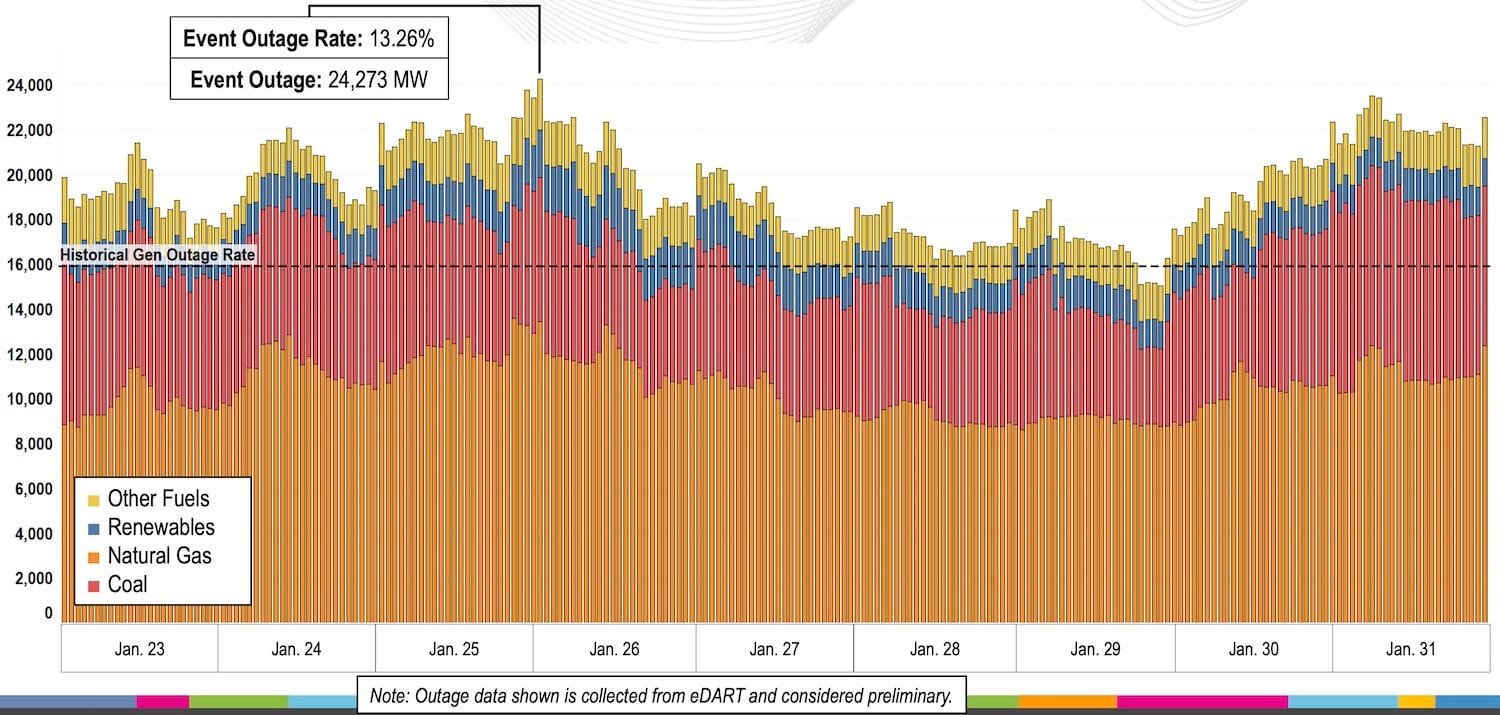

Winter Storm Fern made the point in real time. During the January 23–31, 2026, cold weather event, PJM lost over 24 GW of generation capacity — a 13% event outage rate — primarily from plant equipment failures exacerbated by extreme cold.

PJM — Generation Performance (January 23–31, 2026)

Source: PJM.

PJM issued pre-emergency load management actions specifically for the BGE, PEPCO, and Dominion zones — the data center corridor — and the Department of Energy issued multiple Section 202(c) emergency orders.

The first granted emissions waivers covering ~39 GW of grid-connected generation; PJM dispatched 15 generators under this order for a total of 1,035 run hours, providing 5.2 GW of capacity.

The second authorized grid operators to conscript behind-the-meter backup generators at data centers and industrial sites — an order PJM did not ultimately need to implement, but one it had proactively requested.

That PJM sought the authority to call on a generation fleet it does not regulate, during the most severe sustained cold event since the 1990s, is itself a signal of how deeply behind-the-meter capacity has become embedded in regional reliability planning.

Real-time electricity prices in the Dominion zone spiked to $1,800/MWh, against $400–$700/MWh across the rest of PJM. The grid operator whose capacity auction had cleared at $269.92/MW-day for the 2025/2026 delivery year required DOE emergency authority to keep the lights on — and had positioned itself to call on the shadow fleet if conditions deteriorated further.

The implication is structural, not temporary. Data center developers who cannot secure grid power within their construction timelines face a binary choice: delay and forfeit revenue, or generate their own. The economics are straightforward:

A hyperscaler generates $10,000–12,000 in revenue per kW annually

Aeroderivative gas turbines cost $1,700–2,000/kW — a ~$1,500 premium over grid interconnection in unconstrained markets

That premium pays back in roughly two months of foregone hyperscaler revenue

From the lease side, multi-megawatt Northern Virginia hyperscale lease rates sit at ~$130/kW/month, so every month of grid delay is direct lost revenue for colocation providers — and the turbine premium pays back in under a year of lease revenue

Self-generation is not a concession. It is an arbitrage.

II. The Shadow Fleet

The scale of behind-the-meter generation in Northern Virginia is larger than most market participants realize. It spans three categories of infrastructure — each with different economics, different regulatory exposure, and different implications for the communities surrounding them.

Diesel Backup at Scale

Loudoun County alone has approximately 4,700 diesel-fueled backup generators at data centers, permitted by the Virginia DEQ under air permits designed for emergency use — periodic testing, maintenance, and response to sudden grid outages. They were not designed for the role PJM assigned them in summer 2025, when data centers were authorized to run backup generators for up to 50 hours during the heat wave.

Source: JLARC.

The fragility of this arrangement is well-documented. A recent study by JLARC — Virginia’s nonpartisan legislative oversight body — found that if data centers run backup generators longer than normal testing cycles, they reach their annual emission limits within days. PJM’s grid stress events are converting an emergency fleet into a de facto peaking fleet — one that was never permitted to operate that way.

The aggregate exposure is substantial. Virginia DEQ has permitted nearly 9,000 diesel-fueled generators statewide for data center backup, approximately 4,700 of them concentrated in Loudoun County with a combined capacity of 12 GW. These generators currently account for less than 4% of Northern Virginia’s nitrogen oxide emissions — but only because they run at roughly 7% of permitted capacity. JLARC calculated that if all generators ran at their permitted limits, the region could see up to 9,000 tons of nitrogen oxides annually — equal to roughly half of what all sources in Northern Virginia typically emit combined.

The risk is not only environmental — it is regulatory. Under EPA’s Subpart ZZZZ, emergency stationary reciprocating engines may run without hourly caps during genuine grid emergencies, but non-emergency use — including reliability dispatches like PJM’s summer 2025 directive — is capped at 50 hours per year. Engines that exceed that threshold lose their emergency classification and become subject to the full emissions standards applicable to non-emergency units, including continuous compliance monitoring and potentially Title V permitting. A single prolonged grid stress event can convert a facility’s entire backup fleet from a permit-exempt asset into a federally regulated one.

Natural Gas Turbines as Baseload

The diesel fleet is the legacy system. The frontier is natural gas.

Vantage Data Centers received a DEQ permit in 2023 to install eight Titan 130 gas turbines (manufactured by Solar Turbines, a subsidiary of Caterpillar) at its Sterling, Virginia facility — permitted to emit over 160 tons per year of particulate pollution, compared to fewer than 10 tons per year for a typical Loudoun County data center.

Source: Loudoun County.

Vantage II is operating these turbines not as backup but as its primary power source, entirely off-grid. A second data center reportedly twice the size is in planning.

The pattern extends beyond Virginia — though not always outside regulatory view. Meta’s data center campus in El Paso, Texas — planned for 1 GW at full buildout — will power its accelerated second phase with 813 modular natural gas generators totaling 366 MW, a $473 million facility funded entirely by Meta but owned by El Paso Electric, operating off-grid during an initial five-year “bridge period.”

Source: Meta.

The El Paso City Council voted unanimously to intervene in the regulatory process, citing concerns the generators could eventually be rolled into the general rate base.

That El Paso’s structure — utility-owned, publicly debated, subject to regulatory intervention — contrasts sharply with Northern Virginia, where comparable onsite generation operates with no utility involvement and no equivalent public process.

The capital markets are moving in the same direction. Blackstone — which controls approximately 1,000 MW of data center load in Virginia through QTS Data Centers and a joint venture with Digital Realty — acquired the Potomac Energy Center, a 774 MW natural gas power plant, for $1 billion, positioning itself to fuel behind-the-meter generation at its own facilities.

Local regulators are beginning to respond. The Loudoun County Zoning Administrator determined in the American Real Estate Partners’ Arcola Grove case that onsite gas turbines constitute a separate principal use, not an accessory use to the data center — a distinction that subjects new installations to the full land use review process, including public hearings, environmental review, and Board of Supervisors approval.

Source: Loudoun County.

But existing facilities that installed turbines before this determination were not retroactively reviewed. During opening disclosures at the March 12, 2026 Loudoun County Planning Commission work session, the Commission Chair reported that applicant representatives — from Cooley and Ardent — had recently met with him regarding an upcoming application for a gas turbine power plant intended to power a couple of data centers — signaling that standalone onsite generation facilities, separate from the data centers themselves, are entering the development pipeline.

The Bridge Power Argument

The industry’s preferred framing is that onsite generation is transitional — “bridge power” deployed to meet construction timelines, then converted to backup once grid service arrives. Multiple operators, including xAI, Crusoe, and CoreWeave, have explicitly structured their onsite deployments around this Bring Your Own Generation (BYOG)-to-backup conversion strategy.

Because AI training workloads are inherently fault-tolerant — GPU clusters checkpoint frequently enough that the full 2N power redundancy of a traditional enterprise data center is unnecessary during bridge operation — the economics are attractive: operators skip the diesel generator procurement cycle entirely, deploying the same turbines first as primary power and later as backup, reducing total lifecycle capital expenditure per MW.

The argument deserves acknowledgment, but not credulity. If grid delivery timelines run 4–7 years then “bridge” periods produce years of unregulated baseload emissions from equipment permitted as backup. The regulatory gap does not close because the operator intends to connect to the grid eventually. It persists for as long as the grid cannot deliver.

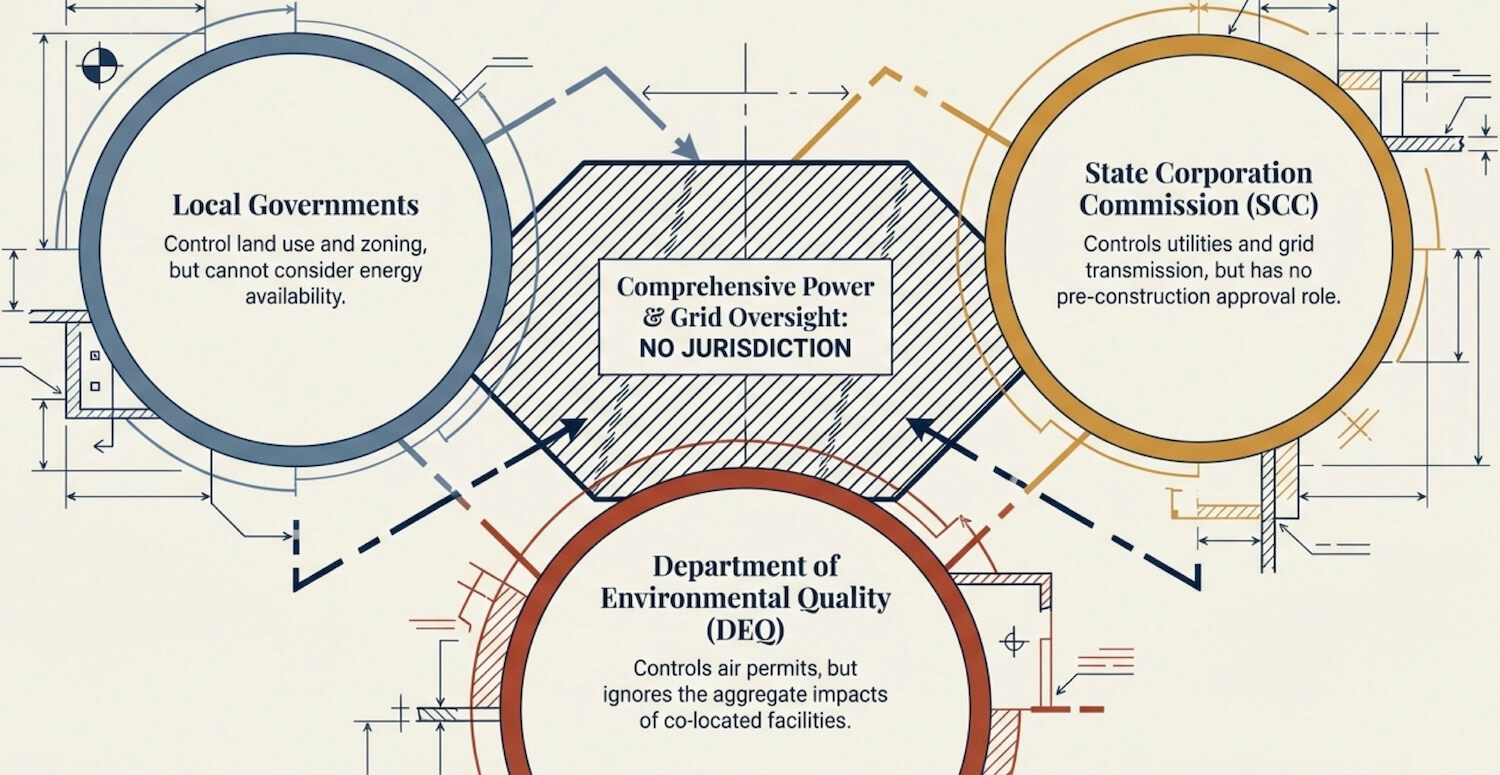

III. The Regulatory Vacuum

The core problem is not that onsite generation exists. It is that no single regulatory authority governs its aggregate impact.

Three Regulators, Zero Overlap

Virginia’s oversight of data center power is split across three bodies, each with jurisdiction over a different slice — and none with jurisdiction over the whole.

The State Corporation Commission (SCC) regulates electric utilities, transmission siting, and grid interconnection — but has no role in approving data center construction before it happens. Once a locality approves a data center, the utility has a legal obligation to serve it, and the SCC’s involvement is largely after-the-fact through rate cases and transmission siting. If a data center builds its own power plant and never connects to the grid, the SCC does not regulate it.

The Department of Environmental Quality (DEQ) issues air permits for stationary sources, with the majority being Minor New Source Review permits. Individual onsite generators — whether diesel backup units or natural gas turbines — are classified as minor sources based on facility-level emissions, not the aggregate impact of thousands of units across co-located facilities. Nearly 9,000 backup generators have been permitted statewide, with approximately 4,700 in Loudoun County alone. DEQ has stated it is conducting further study of localized air quality, but has never performed a cumulative impact analysis of these co-located sources.

Local governments regulate land use, zoning, noise, and site design — but Virginia’s regulatory structure has historically not authorized them to consider energy or power availability when approving data centers. No explicit prohibition exists in statute, but grid impacts are not evaluated in any public process before local zoning approval, and once a data center is approved, the utility is legally obligated to provide service regardless of grid strain. Virginia HB 1112, introduced in the 2026 session, would have empowered local governments to consider current power availability and deny applications where electric energy is insufficient, while also allowing utilities to delay service until local approval is granted. However, the House Committee on Counties, Cities and Towns stripped the bill’s enforcement provisions and continued it to the 2027 session.

The practical result is a complete regulatory gap. A developer can build a facility with onsite gas turbines as primary power, receive a minor-source air permit from DEQ, never connect to the grid, and receive land use approval from a county with no authority to ask whether the grid can serve the site. The aggregate environmental impact of hundreds of such facilities in a single corridor is no one’s responsibility.

The gap is now being institutionalized from above. In 2025, PJM fast-tracked its Critical Issue Fast Path for Large Load Additions (CIFP-LLA), a process that would classify data centers exceeding 50 MW as “non-capacity-backed load” unless they secured their own dedicated generation or agreed to curtailment during peak demand. Before PJM could file, FERC moved first — issuing a December 2025 order finding PJM’s existing tariff “unjust and unreasonable” for co-located large loads and capping behind-the-meter generation at 50 MW. But the cap applies only to co-location — loads sited at existing grid-connected plants.

In January 2026, PJM’s Board formalized a partial response: a “Bring Your Own New Generation” (BYONG) framework offering expedited interconnection for load-paired generation. PJM’s subsequent March 2026 filing at FERC specified that developers using the expedited track would bear 100% of necessary network upgrade costs.

BYONG creates an orderly on-ramp for facilities that choose to interconnect — but nothing compels off-grid operators to use it. Facilities that generate their own power and never interconnect, like the model proliferating in Northern Virginia and El Paso, remain outside PJM’s tariff authority entirely.

Noise as a Leading Indicator

Noise is the canary in the coal mine for the broader regulatory response. Loudoun County’s current ordinance sets a 55 dBA standard at the property line — designed for intermittent industrial noise, not the continuous tonal output of data center cooling systems and onsite gas turbines. The EPA recommended a 45 dBA residential threshold in 1974; a 10 dB difference represents a 10× increase in sound intensity — perceived by the human ear as roughly a doubling of loudness.

Vantage II’s turbines are audible from over 1,200 feet. A county Supervisor testified that homes 1,650 feet from a data center in Sterling, Virginia can hear backup generators clearly, and those 350 feet away can hear them “clear as day.”

Neighboring jurisdictions are already acting. Prince William County adopted a comprehensive noise ordinance in October 2025 — effective May 1, 2026 — establishing a C-weighted scale for steady tonal low-frequency noise with dedicated enforcement staff. Loudoun County has engaged engineering firm WSP as a noise consultant for its Phase 2 data center standards, with noise identified as the “most important” element.

For investors, the signal is clear: noise regulations are the leading edge of broader environmental tightening. Where noise ordinances tighten, emissions regulations follow.

IV. The Emissions Blind Spot

The environmental data tells two contradictory stories, and the discrepancy itself is the finding.

Industry groups, citing DEQ data and the JLARC data center study, note that data centers contribute only 9% of Loudoun County’s total DEQ-reported air pollution and are using only 7% of their DEQ air permit capacity. They argue the emissions profile is modest relative to economic output. But the Metropolitan Washington Council of Governments (MWCOG) tells a different story at the regional level: Loudoun County has the highest gross emissions increase in the region — 130% — and the highest net increase — 145%. Data center emissions more than doubled between 2020 and 2023.

MWCOG — % Change in Gross GHG Emissions, 2005-2023

Source: Metropolitan Washington Council of Governments.

Both sets of numbers are true simultaneously — they simply measure different things. DEQ measures facility-level permitted emissions against permit thresholds. MWCOG measures actual aggregate emissions across all sources in a geography. The gap between these two frames — between what is permitted and what is emitted, between the per-facility snapshot and the corridor-level trend — is precisely where the environmental risk sits. The 9% figure captures the current share of the county’s pollution budget. The 130% increase captures the trajectory of change.

For investors underwriting 10–20 year infrastructure assets, the trajectory is the relevant number.

V. Who Pays for the Grid That Data Centers Are Leaving?

The onsite generation trend creates a second-order problem at least as consequential as the environmental one: cost allocation.

When data centers bypass the grid, they avoid paying for the transmission infrastructure built to serve them — but that infrastructure still gets built, and its costs fall on remaining ratepayers. In February 2026, the PJM Board approved $11.8 billion in new transmission system enhancements, driven primarily by data center load growth across the AEP, Dominion, and PPL zones.

Separately, a Union of Concerned Scientists analysis of data center transmission connection costs — a narrower category than total system enhancements — found that 95% of the $4.3 billion assigned in 2024 were socialized across all ratepayers, with only 5% directly charged to the requesting customer.

Virginia is beginning to respond. The SCC created a new rate class in November 2025 — GS-5, for users of 25 MW or more — effectively targeting data centers. Two 2026 General Assembly bills attacked the cost problem directly: SB 253 would assign PJM capacity and distribution infrastructure costs for customers above 25 MW to the high-usage class, raising their rates and reducing general population rates by approximately 3%; SB 339 directs the SCC to determine by January 1, 2028 whether Dominion’s generation and distribution costs unfairly burden non-data-center customers.

The rate trajectory is steep.

SCC rate recovery: The SCC approved $775.6 million in Dominion rate increases for 2026–2027, adding approximately $13.60 per month to typical residential bills — costs driven largely by infrastructure buildout for data centers that are increasingly bypassing the grid entirely.

Dominion bill trajectory: Dominion’s own filings project average residential bills reaching $256 per month by 2035 under Company methodology and $309 under the SCC’s directed methodology, up from $160 in late 2025 — a 5%–6.5% cost trajectory CAGR that strengthens the economic case for large loads to self-generate rather than remain on the system.

PJM capacity market: PJM capacity prices surged from $28.92/MW-day in 2024/25 to $269.92 in 2025/26, then hit the FERC-approved cap in both 2026/27 ($329.17) and 2027/28 ($333.44) — while falling 6,516 MW short of reliability requirements for the first time — with data centers accounting for nearly 5,100 of the 5,250 MW increase in PJM’s forecast peak load between the two most recent capacity auctions, concentrating infrastructure costs on remaining ratepayers.

The Defection Spiral

The cost allocation problem is also reflexive. As data centers leave the grid, the fixed costs of transmission and generation capacity concentrate on a shrinking base of remaining ratepayers — making grid power more expensive and strengthening the economic case for the next facility to self-generate. This is the utility “death spiral” that regulators have studied in the context of distributed solar, but data center defection operates at hundred-megawatt scale in quarters, not kilowatt scale over decades. If rate increases under SB 253 and GS-5 make grid service less competitive relative to onsite generation, the legislation designed to correct the cost imbalance could accelerate the very defection it seeks to address.

The investment implication is direct. Developers who build onsite generation avoid grid power costs but still rely on the grid as backup. If rate structures shift to impose higher standby charges on behind-the-meter generators — as utility commissions in several states are now considering — the economics of onsite generation change materially. FERC’s December 2025 order requiring PJM to create clearer tariff rules for co-located loads signals that the federal level is moving in the same direction.

VI. Pricing the Transition

The rise of onsite generation is not a temporary response to a grid bottleneck. It is a structural shift in how power reaches compute infrastructure, reshaping the competitive landscape in three specific ways.

1. Grid Access Is Now a Scarce Asset

Facilities with existing grid connections — particularly those with headroom to expand within their current utility service agreement — are worth more than greenfield sites requiring new interconnection. The timeline from interconnection application to commercial operation has stretched from under two years in 2008 to over eight years as of 2025, and upgrade costs have escalated from $29/kW in 2017–2019 to $240/kW in 2020–2022. For capital allocators, an existing grid connection with expansion headroom is a years-long head start that no amount of capital expenditure on onsite generation can fully replicate.

2. Onsite Generation Changes the Cost Equation

A data center with onsite gas turbine generation is a fundamentally different asset than one served by the grid. The all-in capital cost of onsite combustion generation now ranges from $1.2 million to $2.5 million per MW of installed capacity — with aeroderivative gas turbines at $1,700–2,000/kW, industrial gas turbines at $1,500–1,800/kW, and reciprocating engines at $1,700–2,000/kW. Fuel cells, at $3,000–4,000/kW, remain a higher-cost alternative. This compares with grid interconnection costs that historically ran $0.1–0.3 million per MW in unconstrained markets.

If the market is not comparing these assets on an apples-to-apples basis, published cost benchmarks may understate the true all-in cost of new capacity in grid-constrained markets.

3. The Regulatory Window Is Closing

The regulatory framework that allowed this shadow power system to grow — where no single regulator covers the whole — is unstable. Loudoun County has adopted Tier 4 generator mandates — the EPA’s strictest emissions standard for diesel engines, requiring exhaust aftertreatment that significantly increases per-unit cost. Prince William County has adopted a comprehensive noise ordinance. The SCC has created a new rate class targeting high-usage customers. DEQ is conducting a 3-year air quality study. JLARC recommended formalizing utilities’ ability to delay service when capacity is insufficient.

None of these individually closes the regulatory gap. But the sheer volume of activity is itself a signal: Loudoun County is tracking 18+ data center-related bills in the 2026 General Assembly session alone — covering noise authority, water disclosure, onsite generation, Tier 4 incentives, waste heat, and energy storage. Collectively, they signal a tightening that developers should price into 5–10 year project economics.

The convergence points are identifiable: DEQ’s air quality study is expected to conclude by late 2027 or early 2028, potentially redefining whether clustered onsite generation qualifies as a major pollution source. Loudoun County’s Phase 2 data center standards — covering noise, onsite generation, microgrids, and energy storage — are projected for completion in Spring 2027.

The Bottom Line

The U.S. data center industry is building a shadow power system — behind-the-meter, behind-the-permit, and behind the awareness of most market participants. In Northern Virginia alone, that system includes 4,700 diesel generators, certain facilities running entirely on jet turbines off-grid, and the world’s largest alternative asset manager that acquired its own gas power plant.

This is not sustainable, and the market is beginning to respond. Tier 4 mandates, dedicated rate classes, noise enforcement, cost allocation legislation, and a pending DEQ air quality study are all converging on the same target. The developers who will be best positioned are those voluntarily adopting Tier 4 generators, committing to GIS substations, and securing grid interconnection — not because the current rules require it, but because the next round of rules will.

For investors, the question is not whether onsite generation is viable. It is whether the assets being built today under today’s permitting framework will still be compliant — and insurable — under the framework that is visibly emerging.

Measured AI provides institutional-grade analysis of the physical infrastructure powering AI data centers. For access to our full archive, data tools, and weekly briefings, visit measuredai.com.